Marvelous Accrual Basis Of Accounting Example picture

Accrual Basis Of Accounting Example. In the cash method of accounting, revenues and expenses are recorded in the reporting period that the cash payment is made. Accrual Accounting is the most accepted accounting principle which states that revenue is recognized when the sale is done (irrespective of the cash or credit sale) and the expense is matched and recognized along with the corresponding revenue (irrespective of whenever it's paid).

Let's say you own a business that sells machinery.

This is markedly different because it aims to correlate expenses and revenue to help give a greater measure of profitability and business health.

Accrual Accounting Concepts - Financial Accounting ...

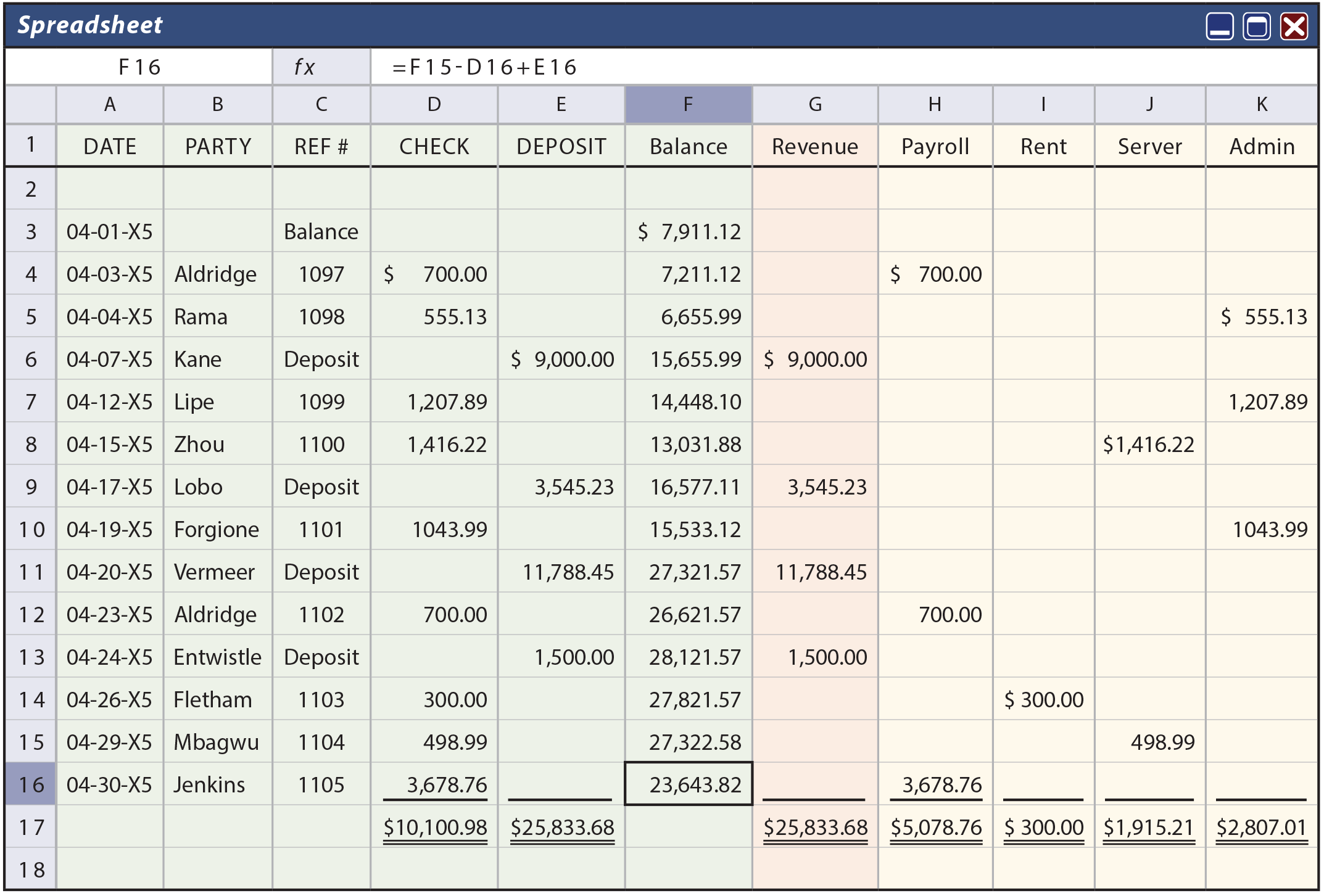

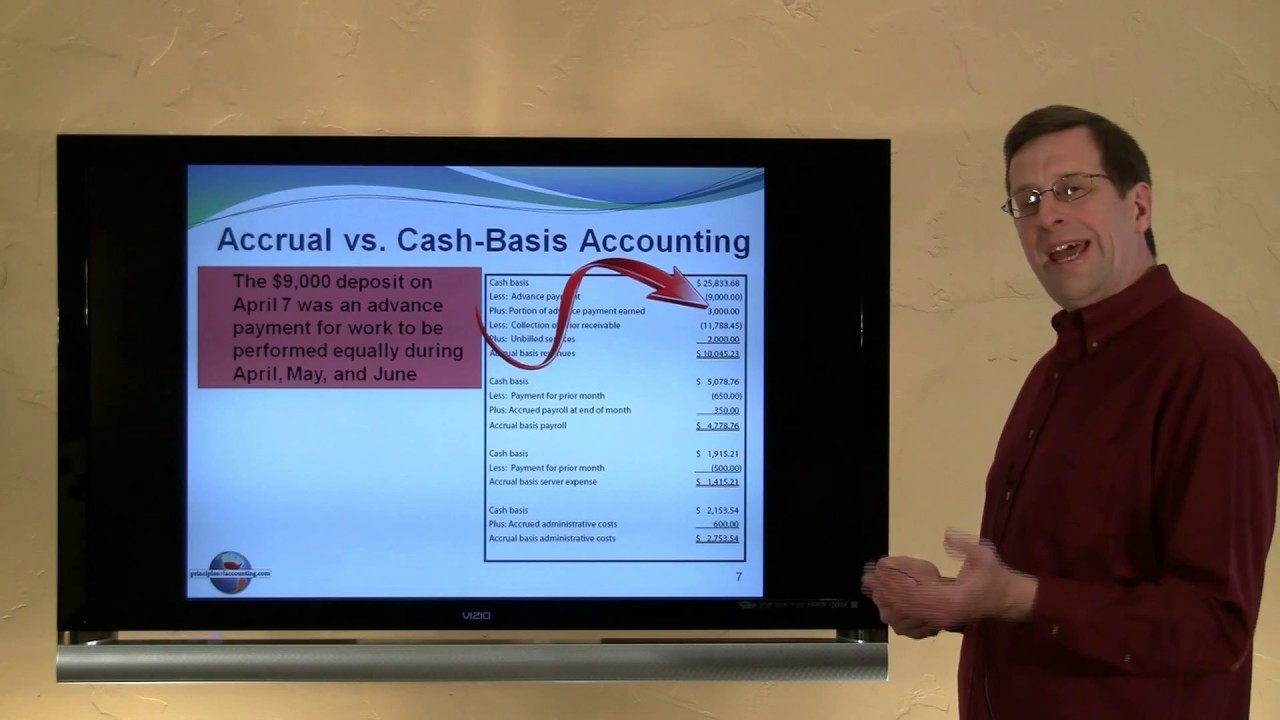

Accrual Versus Cash-Basis Accounting ...

Using Accrual Accounting to Make Financial Statements More ...

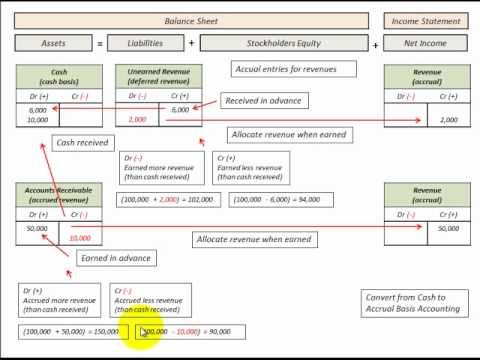

3 - Accrual vs. Cash-Basis Accounting - YouTube

PPT - 2011 AMC INSTITUTE COMMUNITY CONFERENCE ...

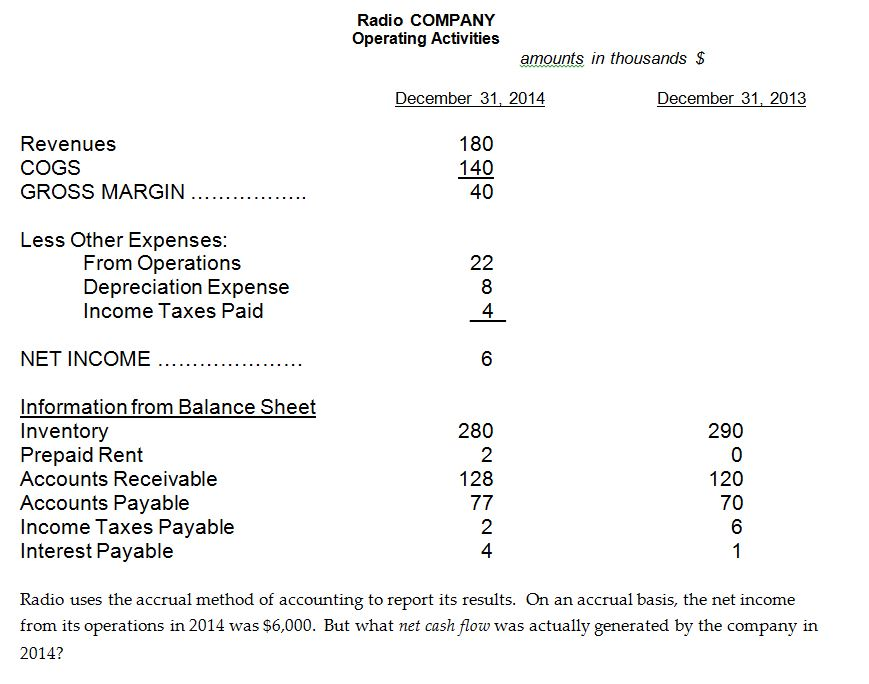

Cash Basis To Accrual Basis Conversion (Accrual And Cash ...

Cash Accounting (Definition, Examples) | How it Works?

Posting When You Use Cash Basis Accounting (Oracle ...

Difference Between Cash Basis and Accrual Basis Accounting ...

Finance Archive | February 08, 2015 | Chegg.com

Cash Basis Vs Accrual Basis of Accounting - Complete Details

Posting When You Use Accrual Basis Accounting (Oracle ...

The Accrual Balance Report

Understanding Accrual to Cash Conversions ??? The Daily CPA

Accrual-Versus Cash-Basis Accounting, Modified Approaches ...

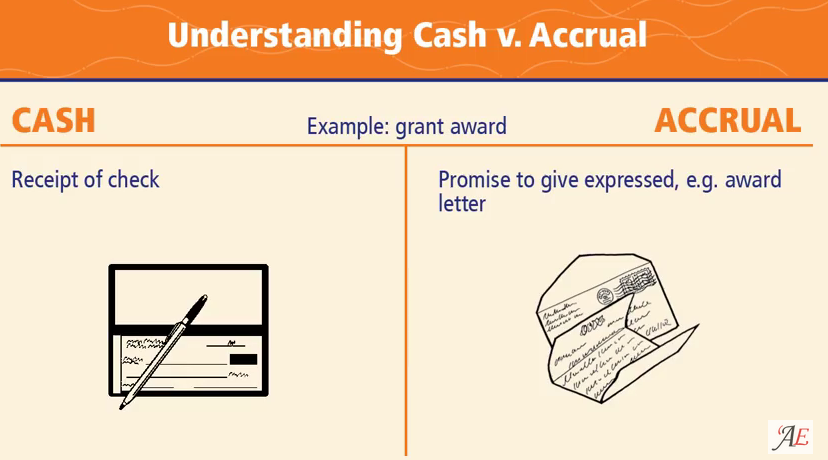

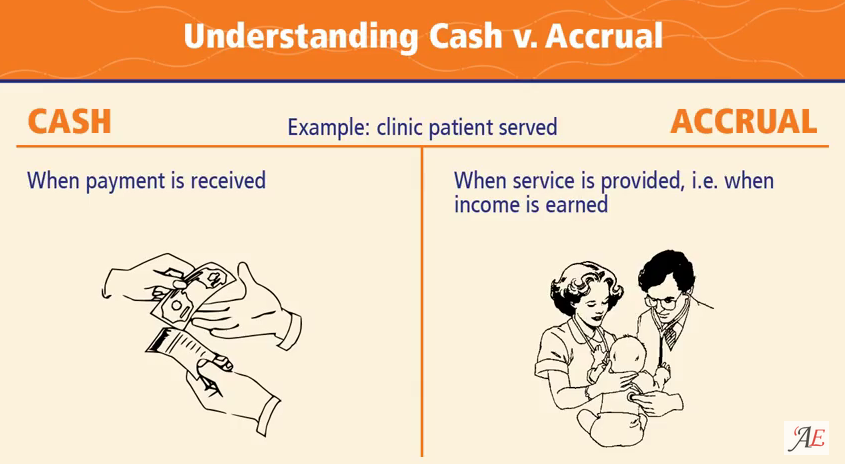

Cash vs Accrual accounting | Accounting Education

Cash vs Accrual accounting | Accounting Education

M.A AUDITS & ACADEMI: Cash vs Accrual accounting

Cash vs Accrual Accounting | Double Entry Bookkeeping

Irish 21st Century Students: Process the Following ...

Under accrual accounting, therefore, both sellers and buyers report revenues and expenses based on each party's first pair of entries. Accounting on an accrual basis is intended to match up revenue and expenses with they are incurred or delivered, without regard to when payment is issued or received. How to Use Cash Basis Accounting Example "Cash Basis" Transaction Records Accrual Basis: The Accrual basis is the accounting principle that use to recognize and records accounting transactions or events in the financial statements regardless of its cash flow.